AUM in Digital wealth is not the metric that lived up to expectations

From 2016, consulting practices put out their 5yr predictions on the growth of the Robo Advisor subsector, mainly focusing on the potential to gather assets.

It was the time when Vanguard was making its first leapfrogging attempts in a space that Betterment and Wealthfront had brought to market. Personal Capital was also shaping up the hybrid version of `digital investing`. Deloitte, CB insights, Aite Group, and others were predicting assets under management by 2020 (which at the time, seemed far away for all of us).

Predictions ranged between $ 2.2 trillion and $ 3.7 trillion in assets to be managed by Robo-Advisory services by 2020 and $16 trillion by 2025.

Permit me to take the mean of the range predicted for 2020 (trillions of USD are being transferred from the government to the `people` anyway as we speak) and round it up to $3 trillion for 2020.

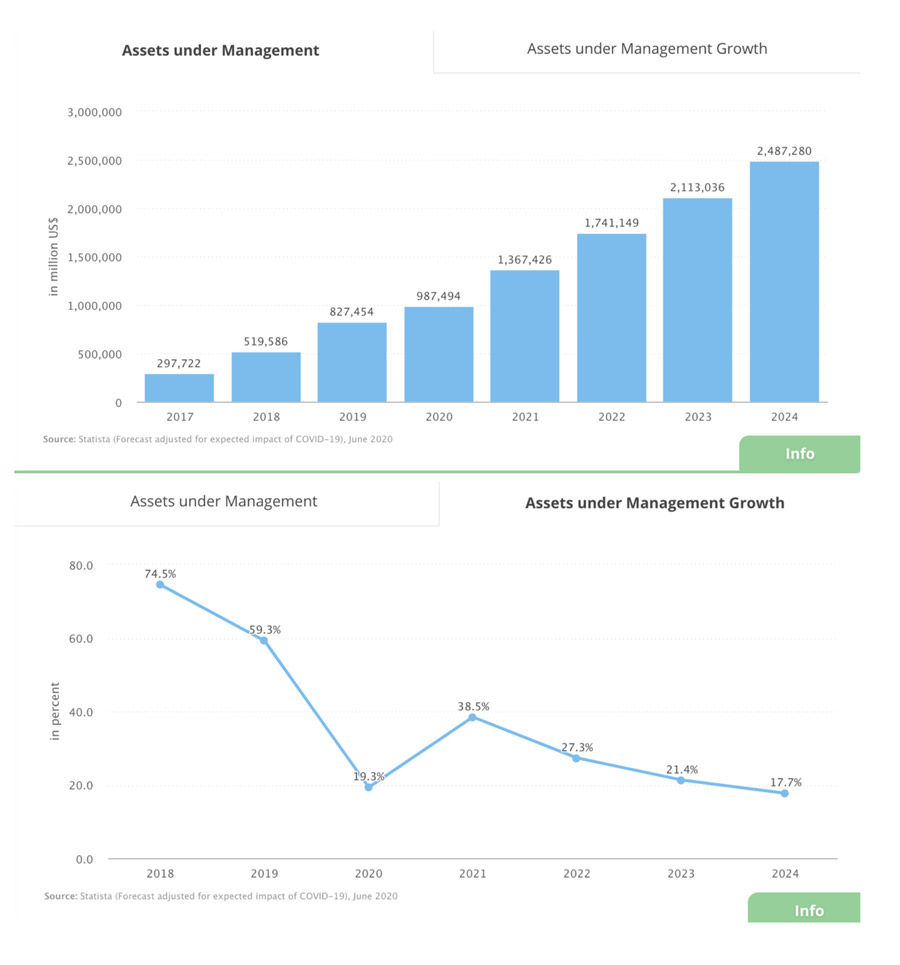

2020 — Well we are in the second quarter of 2020 and we are just reaching $1 trillion. A recent report by BuyShares says we are heading to $987billion. So, we are at 1/3 the 2016 prediction even though the S&P500 is up 30+% and the Dow is up 28+%, since Jan 2017.

What is more remarkable is that the current 5yr outlook compiled by BuyShares and based on Statistica data, predicts that in less than 5yrs the AUM will grow x2.4 times, reaching $2.4trillion.

At first sight, it may seem to you an optimist outlook. It is actually, a heavily discounted view from that set out back in 2016 when the sector started attracting more VC investments and incumbents. The first predictions were from 0-$3trillion in less than 5yrs and then from $3trillion-$16 trillion in the second 5yr phase (x5+ times).

And now this study is saying, let’s cut the 5+ times growth rate in AUM to more than half. And let’s cut the AUM managed over the next 5yrs by 85% (we had said $16trillion and now we say $2.4trillion).

Let’s step back and look into the mirror as if it is 2025. Of course, digital onboarding and automated asset allocation offered currently via ETFs will be 100% an option everywhere and probably free.

The more interesting and meaningful question is about the evolution of the ETF market itself which has been the bread and butter of all the digital investing offerings (lumped under the `robo-advisor` umbrella be it with or without human advisory services); and whether artificial intelligence will actually transform digital investing.

1️⃣ Will `robo-advisors` continue to build their businesses mainly using ETFs? Their low-cost core value-add has been interchangeable seen as a win for passive investing and mainly via indices.

2️⃣ Will the 12% of the $4.7trillion ETF market (based on 2018 year-end data, see here) grow and to what extent?

3️⃣ Will active ETFs grow given the current macro environment? ANTs are just emerging and are a step back from the transparency trend and the zero-commission trend. ANTs are active non-transparent and on average their expense ratio is 70bps. Their position reporting is much better than mutual funds (quarterly). Their cost-adjusted and risk-adjusted-performance will have to be seen going forward. They are currently only 2% of the ETF space (see here).

4️⃣ Will artificial intelligence finally take over the asset allocation and the decision of switching between direct indexing or stock picking or momentum.

A few facts to consider:

1. The ETF space grew sustainably in 2019. Statistica reports $6.18trillion by year-end of 2019. That is a 30% increase. Of course, by the end of Q1 2020, the ETF global industry experienced a c. 16% drop ($5.4trillion) which was 100% due to the drop-in asset values. ETFs actually experienced in Q1 net inflows of c. $120billion. These were inflows during the major March selloff. Source

2. An update on my calculations of the assets under management by digital wealth services points to a c.30% increase (by 2019 year-end), which matches the ETF increase. Source

3. The actual role of artificial intelligence in all the Digital wealth offerings, is still minimal. Even the large incumbents with sizable digital wealth AUM, like Merill Edge or Vanguard, are still in the initial phase of digital transformation in wealth management. Vanguard actually has done very little on the needed digital integration front. Merill Lynch is probably ahead with its new CEW — Client Engagement Workstation — that integrates market data, client information, account servicing tools and some narrow artificial intelligence tools (chatbots).

For 2025, we should be making predictions of the extent that Artificial intelligence will be making better decisions for my asset allocation than I do, or my private banker, or my financial advisor, or my digital wealth service provider.

What has gone wrong in Fintech that pushed the original projections of $16trillion AUM in 2025, to $2.4trillion?

Where are the trillions of currencies that are being transferred, going to end up?

Isn’t the digital transformation of the mutual fund industry what will happen over the next 5yrs? Whether it is through DLT as an infrastructure of the mutual fund administration or by the tokenization of fund structures or the disintermediation of the European banks who dominate mutual fund distribution or all of the above? And won’t all this lead to an exponential growth of the `Digital wealth` AUM?